Introduction

The adoption of artificial intelligence (AI) throughout the economy will have a profound impact on society. However, some misconceptions about the recent breakthrough need to be addressed. Firstly, AI is not as new as many believe. Secondly, it may not be as widely applicable as first thought. Thirdly, the extent of the AI bubble is uncertain, but its existence does not imply that the technology will prove to be unprofitable. After working through these topics, we will look at how AI will fit into the Winnipeg/Manitoba economy.

Timeline of AI progress

Alan Turing, the father of computer science, proposed the Turing test, or imitation game, which involves a computer attempting to convince a human being that it is human. He believed that once a machine could win the game it was considered intelligent. In the 1950s, Frank Rosenblatt began working on image recognition technology with the intent of creating an intelligent machine. Specifically, he wanted to train a computer to identify the gender of a person by analyzing their picture (a simple headshot). To do this, he used a basic neural network that was modelled off the neural network of the human brain.

While he was not successful in his attempt, Geoffrey Hinton (who shared the 2024 Nobel Prize in Physics for his work related to AI) believed that Rosenblatt’s neural network approach was correct but required enhancement. Hinton and his colleagues began their work in the 1980s but, like their predecessors, were throttled by data limitations and computer processing power. In the 1990s significant progress was made in computing power, and information was rapidly being uploaded onto the internet. With these advancements the neural networks had both the data and the hardware they required to begin training themselves.

Portrait of Geoffrey Hinton, Nobel Prize Organization

In 1997, the AI program Deep Blue defeated the Chess Grandmaster and former world champion (1985 – 2000) Garry Kasparov in a six-game chess match by winning two games and drawing three. Less than 15 years later, image-recognition AI technology, first developed by Rosenblatt nearly 60 years prior, outperformed humans for the first time. The next breakthrough occurred when the AI program Alpha Go (which plays the strategy board game Go) defeated the world's Go champion, Lee Sedol, with a score of 4 - 1 in their first match in 2016. Finally, in 2022, the now infamous ChatGPT large language model (LLM) was released by OpenAI, thus ushering in the new era of widely accessible and affordable AI technology.

What jobs can and will AI do?

Estimates of how much AI technology will increase productivity vary from source to source. Goldman Sachs estimates that it will increase productivity by somewhere between 12 – 15% over the next decade. Daron Acemoglu, who shared the 2024 Nobel Prize in Economics, reckons the impact on productivity will be much smaller, at less than 1% over the next 10 years. He and his co-author, Pascual Restrepo, answer two questions when investigating the labour market impact of AI: how complicated are the tasks people do? And what specifically will AI be contributing to the task?

For a computer, a task is either easy or hard. Beating Magnus Carleson, who is presently the best chess player in the world, is considered an easy task because it is perfectly objective in that the actions — moving the chess pieces around the board — are well-defined and directly connected to the outcome — winning or losing the game. Plus, there are hundreds of years of recorded chess matches that the computer uses to train itself. A hard task is one where the connection between action and outcome is very weak and/or the amount of data available to the computer is limited. For example, writing this Digest involves the action of organizing words together into a single text, but the outcome of successfully engaging with and maintaining or expanding the reader base is not well defined or observed. So, according to Acemoglu and Restrepo, AI will have a better time with easier tasks - meaning we can assign it those jobs based on assessed difficulty.

Easy or hard, Acemoglu and Restrepo sort the contributions AI will make to tasks into four categories:

- Automation: tasks previously done by humans will be completely performed by AI.

- Complementary: AI will assist humans with their tasks but is unable to complete the task in its entirety.

- Automation deepening: tasks that are already automated, by AI or not, will be further automated by AI.

- New tasks created by AI that will improve the production process.

The automation and complementary categories are believed to be the most common within AI deployment today and, in theory, will replace some workers and make others more productive. If the assistance provided by AI is such that fewer people are needed to complete a task, then it is implicitly replacing people in that role - even though the AI cannot perform the entire task. Whether a firm decides to lay off workers or assign them to different tasks is unclear. What is clear is that the task has become less costly than it was, and workers will either have extra time available to allocate to new tasks, or they will move to different jobs. In either scenario, the firm has become more productive through the adoption of AI!

If AI is better suited for easy tasks, and complements (rather than replaces) existing labour, then the impact of AI is going to be concentrated in a small set of tasks within the economy. This means AI’s impact on aggregate productivity, though large for a minority of firms, may be rather small. Additionally, this simple two-pronged approach of task type and contribution type fails to account for the time costs of delegating tasks to AI and processing the output it produced.

The Economist, Ryan Gillet

In the same way that any computer program needs input, so does AI. Someone familiar enough with the required task will have to prompt the AI. Ideally, this will be a part of the preexisting task process, and the AI is just completing intermediate steps on the workers' behalf. However, it may be the case that organizing the task so that AI can understand it actually takes up more time than doing the task itself. Furthermore, even if it does not take an onerous amount of time to prompt the AI, it may still take an onerous amount of time to review the work it completes. Then, once the work is deemed acceptable, it is sent up or downstream for workers, senior management or executives to process. There will be questions about the output, and the answer might be, “The AI did it.” This could spark a debate between decision makers because it is not at all obvious how much trust you can place in the output of AI when it has a known tendency to hallucinate. These additional time costs may shrink the number of tasks AI can complete economically even further than what Acemoglu and Restrepo predict. In addition to the productivity benefits, it is worthwhile to consider the long-term implications of replacing employees with AI. The value of entry level workers goes beyond what they can accomplish today, because these new employees are the senior specialists, managers and executives of tomorrow. Each of the entry level positions replaced by AI reduces the pool of future leaders that can be developed from within the organization. Nonetheless, it is worth exploring examples where AI adoption in the workplace has done well and not so well.

AI can write basic computer programs. In fact, AI has gotten so good at this type of programming that it is taking entry-level work away from new computer science graduates. For harder, more subjective tasks, AI can struggle because it has a tendency to hallucinate. This happens when the language model does not have sufficient data to predict the next word in a sentence and then makes an uneducated guess on what should come next. This sets off a chain reaction of uneducated guesses which leads the program completely astray. As an example, AI note takers are being used in the workplace, but they are prone to errors which includes wrongfully assigning work to people who were not in the meeting and adding in conversations that never took place. Additionally, a study by the Yale School of Management found that 95% of the 52 companies they interviewed did not see productivity benefits from AI adoption. To be fair, these programs are still relatively new and should see improvement going forward. How much they can improve is what people are speculating on. If you are skeptical about such claims and aware of the present limitations of the technology, there is good cause to question if the amount of investment in AI is irrational or not.

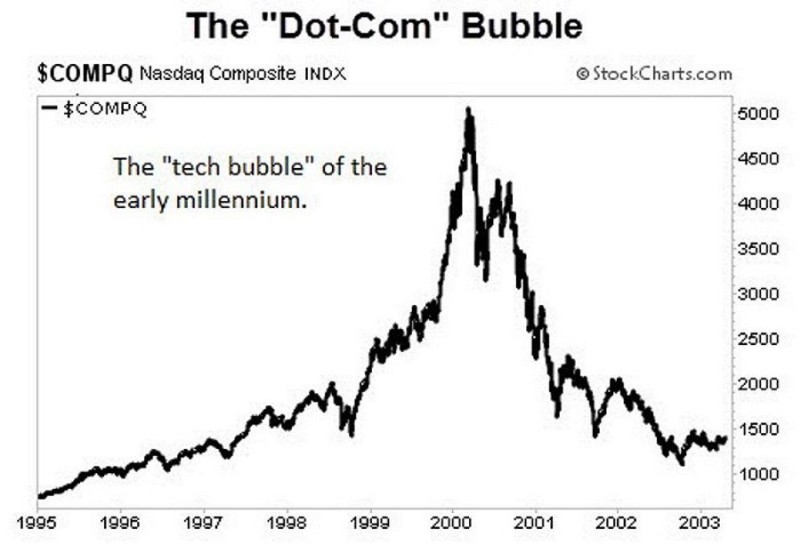

What we can learn from the dot-com bubble?

Investopedia

The AI boom is comparable in many ways to the dot-com bubble — which burst more than 25 years ago in February 2000. The dot-com bubble was the result of the commercialization of the Internet which saw existing firms, such as IBM, Microsoft and the Canadian giant Nortel (which went bankrupt in 2008) pouring billions into infrastructure and acquisitions and the emergence of startup companies that were completely overvalued, such as Pets.com (which went bankrupt in November of 2000, nine months after it went public).

Though the bursting of the dot-com bubble destroyed both incumbent firms and startups, many firms did not just survive the crash but thrived after the dust settled. Amazon was six years old when the bubble burst, and it went on to become the world’s most valuable company in 2019. Alphabet (formerly Google) started in 1998, two years before the crash, and is now a tech leviathan. In the following years, there was still a healthy stream of new Internet-focused tech companies. Meta (formerly Facebook) started in 2004, while X (formerly Twitter) started two years later in 2006. The video and streaming industries boomed in the 2010s (Netflix, Twitch, YouTube etc.).

Despite the over-investment in dot-com companies, the exaggerated claims of their business models and the hysteria that followed, the internet was a major technological accomplishment that contributed trillions to global GDP, created jobs and forever changed society (for better or for worse). It stands to reason that, should the AI bubble burst, many of the existing companies today will survive the crash, and new innovative firms will still develop in the future. The problem is that no one knows how big the bubble is, when it will pop and what the implications of its collapse will be – a slow deflation, an abrupt implosion or something in between.

We can look at several indicators to assess the severity of the AI bubble: the price-to-earnings ratio (P/E) of companies (which is simply the price of a company's stock divided by earnings per share), the overall finances of the AI industry and its investors, how concentrated the stock market is in AI, and the valuation of AI companies (not just their stock price). Analysts at Goldman Sachs emphasize that the P/E ratio of the Magnificent 7 (Alphabet, Amazon, Apple, Meta, Microsoft, NVIDIA and Tesla) is just over 50 per cent of the P/E of the dot-com bubble leaders (Cisco Systems, IMB, Intel, Lucent, Microsoft, Nortel and Oracle) right before the downturn; and they have more cash and less debt than the dot-com bubble leaders did before the market crashed. So, not only are the stock prices of the leading tech companies today more balanced than their dot-com predecessors, but so are their finances. However, other indicators are sending different signals, including valuation and market concentration.

In April of 2024, the combined value of the Magnificent 7 exceeded 30 per cent of the S&P 500 and has not dropped below that threshold since. Just before the bubble burst in 2000, the dot-com bubble leaders combined value was less than 15 per cent of the S&P 500. Though the business portfolios of the Magnificent 7 are diversified beyond AI, the market is putting a lot of money into these top companies, more so than it did in the dot-com era. This is a red flag because, if the AI investments are less profitable than projected, the Magnificent 7 share prices will drop when one or several factors finally spook the market, and that decline will spill over into the rest of the economy. The extent of the drop, and its effect on the rest of the economy, will depend on how much the market has overestimated the potential of AI – which is impossible to determine until the adjustment occurs.

Recently Orlando Bravo, an investor worth billions, has stated that he believes AI companies are overvalued and compared the present market to the dot-com bubble. Though, like the Goldman Sachs report, he admits the underlying finances of the market are healthy. Micheal Burry, who famously predicted the 2007-08 housing crash in the US, has bet $1.1 billion on both the NVIDIA and Palantir stocks falling in value. For another example of potential overvaluation, look at OpenAI. It is valued at $500 billion USD despite having an annual revenue of just $14 billion USD and an unprofitable subscription rate of $200 USD per month.

At the other end of the industry, there is a lot of excitement (or perhaps exuberance). Even with all the doubt circling hanging over the industry, AI startups raised more money in the first half of 2025 than they did in 2024, where nearly two-thirds of venture funding in the US (high risk investments) went to AI firms. It appears that, from a valuation and market concentration standpoint, we may be on the precipice of the AI bubble, but the P/E and the balance sheets of the AI industry suggest otherwise. It is unclear how to weigh these indicators against each other. What we can do is peer under the hood by investigating the supply chain of the industry.

AI services companies outsource their computing requirements to the cloud-based data centres (unless, like Amazon and Microsoft, they can pay hundreds of millions to construct and operate their own). These data centres require state-of-the-art hardware, in particular new graphics processing units (GPUs). The GPU companies, like NVIDIA, sell their chips to the data centres (Amazon, Oracle, and Microsoft) who then rent their capacity to the AI service companies (OpenAI). However, NVIDIA has invested billions in OpenAI, who then uses some of these funds to purchase data centre capacity from Oracle, who sources their chips from NVIDIA — thus completing the circle. These circular deals are considered a red flag because they might be artificially propping up the stock prices and valuations of the GPU, data centre, and AI services companies (such as NVIDIA, Oracle, and OpenAI). This is the other side of the over-investment problem: money being directed to the capital stock (data centres and GPUs) and not just the emerging AI service companies.

The dot-com bubble ended with excess capacity of fibre optic cables. Similarly, the AI bubble might result in a period of excess capacity in data centres. This is suboptimal for the economy because there could be several years where supply exceeds demand and that capital could have been allocated to other industries where it would contribute more to GDP growth and job creation.

AI in Winnipeg and Manitoba

The Economist, EBOY

Let us take a quick inventory of AI before we focus on its future in Winnipeg and Manitoba. We know that the technology is not as new as it seems, and this could mean that future progress will come at a more moderate pace if the recent breakthroughs prove to be some of the largest. That progress will be in the form of labour replacing and enhancing AI services which will boost productivity and GDP, but perhaps not by the astronomical amounts first claimed. If the potential of AI services has been overestimated, then the returns to the investment in these companies, data centres and chip designers will be lower than anticipated or even negative. More or less, that is what the bubble bursting would look like: the cash flow of the AI industry (service firms, data centres and chip designers) is less than expected, investors take a loss, the stock market adjusts downwards, some firms in the AI industry go bust, there will be excess capacity in data centres and an oversupply of soon to be outdated GPUs. Yet there will be survivors, new advancements in AI and tangible contributions to GDP.

As with most major economic events, the local Winnipeg and Manitoba economy is diversified enough to absorb the impact of the AI bubble shrinking, deflating or bursting without suffering irreparable damage. Before and after the adjustment, several industries stand to benefit at least modestly from AI services. Industries such as finance, insurance, real estate, logistics (transport, storage, and trade) and information and communication technologies (ICT) cumulatively make up more than 30 per cent of Winnipeg’s GDP. These industries rely on the type of white-collar work that AI can assist with, if not automate outright. This can free up workers for other tasks or allow them to move into new positions altogether.

From a data centre perspective, presuming there is still demand for new facilities in the future, southern Manitoba (which already hosts eight data centers) is an ideal location. Data centres are accessed remotely, so our geographic isolation is less of an issue. There is ample floor space in Winnipeg and the surrounding area to host new data centres; there are a variety of ICT firms already located in Winnipeg that can directly or indirectly support this new infrastructure, and the electricity generated here is low-emission and renewable. With respect to energy consumption, one limiting factor is the amount of excess capacity presently available in Manitoba. In January of this year, Manitoba Hydro set a record for peak electricity demand at 5,111.5 megawatts (MW) when temperatures dipped below –32 C. With optimal conditions, Manitoba Hydro is capable of generating just over 6,000 MW. According to the International Energy Agency, the amount of electricity consumed by a data centre ranges from 10 MW for a small facility, to 100 MW for a larger one. So, there is energy available to power several small- or medium- sized data centres, or a single massive data centre, but for the short term there is not an abundance of energy that can be dedicated to this sector. This means it may not be the top priority for new energy-intensive projects – competing with other local priorities for energy consumption including housing.

Ultimately, we will have to wait and see what AI has in store for Winnipeg, Manitoba, Canada and the rest of the world. The benefits may be less than what some people are hoping for, and they may take longer to be realized. Neither outcome would prove devastating and may actually provide for more economic stability in the short run.

PS: This Digest, and the supporting research, was completed without any assistance from AI whatsoever.